Plan retirement against your trajectory, not the year on your ID.

Two people born the same year can have markedly different remaining healthspans. PensionPulse turns the step data already on your phone into a personalised aging trajectory — and connects it to your retirement plan.

Your aging trajectory and your retirement plan, on one screen.

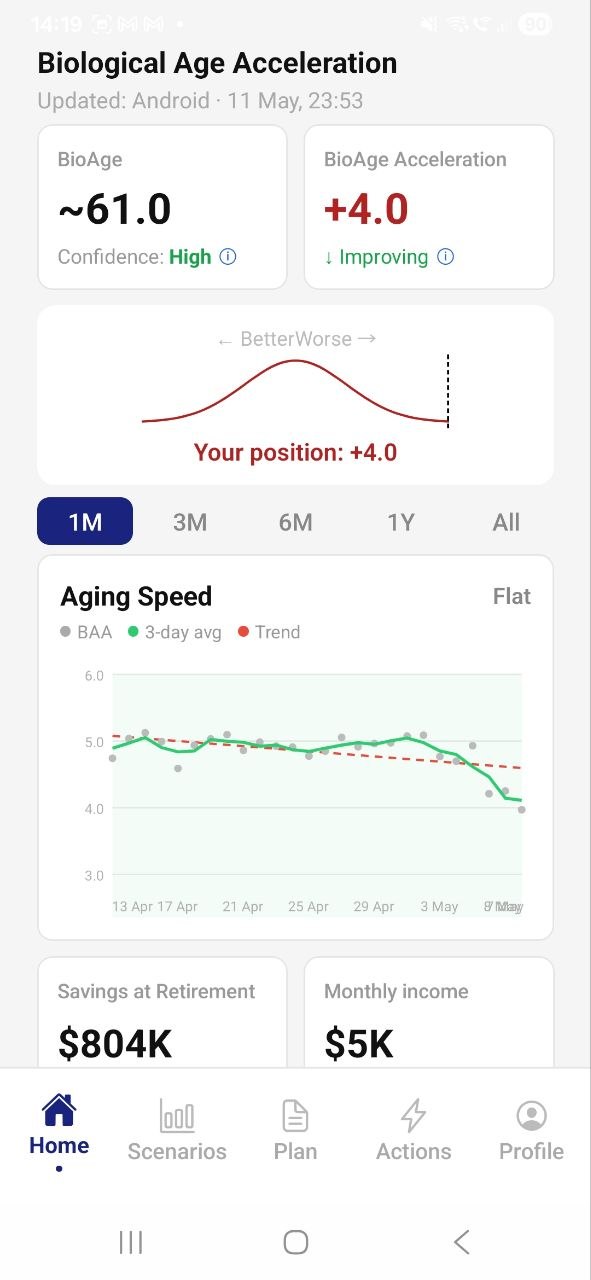

Biological age, aging speed (how far ahead or behind your chronological age you are, in years), and a baseline retirement projection — updated automatically from the step data your phone already collects.

Two readings, two different roles in the plan.

Your physiological state, expressed in years. A 50-year-old can have a biological age of 45 (slower aging) or 56 (accumulated wear and tear). Slow-moving — changes over weeks and months in response to sustained patterns of activity, recovery, stress, and lifestyle.

How far ahead or behind your chronological age your biological age sits, in years, derived from a long-term trend rather than a daily snapshot. 0 means on pace; +4 means biological age four years ahead — body running faster than the calendar; −3 means three years behind — typically the result of sustained positive patterns. The metric that responds to behaviour and closes the feedback loop in weeks, not years.

How each anchor changes when the input is personal.

Traditional planning answers each of these with a single number derived from population averages. With personalised aging information, the answer becomes a range — and the user's position within that range becomes visible.

- No. 01

Planning horizon

TraditionalGeneric ("to 95")PersonalInformed by your personalised projections - No. 02

Payout strategy

TraditionalMost popular: "4% over 30 years"PersonalInputs to weigh lifetime income vs. fixed-term withdrawals - No. 03

Retirement age & SSA benefits

TraditionalAnchored to social or institutional normsPersonalCoordinate career, retirement, and SSA claiming timing - No. 04

Healthcare reserve

TraditionalPopulation-average estimatePersonalRe-prioritised by trajectory

Not a recommendation. None of these reshapings is the product telling the user what to do. Each is a decision the user — together, where applicable, with their advisor — makes. The product's role is to make the input personal rather than averaged, so the decision rests on something closer to reality.

Validated against blood-based and DNA-methylation aging clocks across more than 50,000 activity tracks, and featured in The Lancet Healthy Longevity (2025). The science

One set of indicators, three commercial channels.

PensionPulse reaches its market through three commercialisation channels, introduced in deliberate order. The same indicators flow through all three; what differs is the relationship with the counterparty.

Plan your own retirement.

Your aging trajectory, connected to your retirement plan. Free to start.

Differentiate your practice.

White-label app under your brand. A personalisation layer that creates regular touchpoints with every client.

Enrich your client app.

API-first integration for pension funds, life insurers, retirement platforms.

Six peer-reviewed publications. Validated against external biomarkers.

The methodology rests on patterns within locomotor activity, validated against blood-based and DNA-methylation aging clocks across more than 50,000 individual activity tracks.

Six published papers behind the science. A long-term operating posture for the product.

PensionPulse is in beta. We're inviting individuals, advisors, and pension/insurance providers to evaluate the platform.